What interest expenses are and how to claim them

Interest expenses are tax-deductible business costs. Learn how to calculate and report them on financial statements.

Table of contents

- What are business interest expenses?

- Types of interest expenses

- How to calculate interest expenses

- How interest expenses appear on your financial statements

- Which interest expenses you can claim as tax deductions

- Avoid common mistakes with interest expenses

- FAQs on business interest expenses

Key takeaways

- Interest expenses are the costs incurred to borrow money. Businesses can deduct interest on loans for business purposes.

- There are five main types of interest expenses: loan, credit card, capitalized interest, accrued interest, and bond interest expenses.

- The basic formula to calculate interest is to multiply the loan amount by the interest rate and the time involved.

- Interest expenses appear on your P&L and your balance sheet. They appear as an expense in the non-operating expense section of your P&L. On the balance sheet, any unpaid interest appears as accrued interest under liabilities until it is paid.

- Businesses can often reduce their tax bills by deducting interest on their business expenses from their taxable income. However, the IRS imposes limitations on the interest expenses businesses can deduct for large companies.

- To make sure you’re receiving the deductions you’re entitled to, it’s a good idea to track the interest you’ve paid, record it carefully, and separate your business and personal expenses.

Interest expenses refer to the interest you pay to borrow money or use credit. For businesses, interest expenses are tax deductible, so read on to learn what interest expenses are and how to calculate them, how they appear on your financial statements, and what deductions you can make.

What are business interest expenses?

Interest is the money you pay to lenders for loans, lines of credit, and credit cards, according to the rate of interest the lender charges and the amount you owe them at the time interest is calculated.

Business owners can claim interest as a tax-deductible expense. For example, the $3000 you might pay in interest on your business credit cards during the year is

- a deductible expense that you can claim on your tax return.

- a non-operating expense that you should track in your accounting records so that you can judge the profitability of your business.

Small businesses that use cash basis accounting claim business interest expenses in the year they pay the interest. But, businesses that use accrual accounting claim credit card and loan interest expenses the year they accrue the interest.

Here’s more info on cash basis and accrual accounting

Types of interest expenses

These are the main types of interest expenses.

Loan interest

Interest paid on loans including personal loans, business loans, and mortgages, such as the interest on a mortgage to buy a commercial building.

Credit card interest:

Interest charged on outstanding credit card balances. For instance, a $10,000 balance on a credit card with an annual interest rate of 25%, incurs annual interest of about $25,000.

Capitalized interest

Interest on loans where the interest gets added to the asset's value rather than being deducted right away. This is often done on long-term loans used to finance large, expensive, or long-lasting assets like real estate or manufacturing plants, or heavy machinery.

Bond interest

This type of interest is paid to bondholders (to you or your small business, for example) who’ve bought bonds from governments or corporations as an investment. The government or corporation pays interest to the bondholder and deducts the interest as an expense, while you report the interest as income. The interest on many bonds (such as municipal bonds) is tax-exempt.

How to calculate interest expenses

To set accurate budgets, you’ll need to estimate interest expenses. Here's the simple formula:

Interest = principal x interest rate x time

Let's break it down:

- The principal is the amount borrowed. For example, your flower delivery company takes out a $35,000 loan to buy a refrigerated van – that's the principal.

- The interest rate is the lender’s rate (their charge) to borrow money. Let's say this lender charges you 10% annual interest.

- The time is whatever period you want to calculate the interest over – a year, or the term of the loan, for example.

To estimate the interest on the first year of the loan, for example:

Principal ($35,000) x interest rate (10%) x time (1 year) = interest ($3500).

Or to estimate the interest on the first month of the loan, just change the time period:

Principal ($35,000) x interest rate (10%) x time (1/12 year) = interest ($420).

For precise numbers, use an interest calculator, tax forms, and other tools

This formula gives you a simple estimate of interest over a certain time period. However, it won’t give you a precise amount of interest expense as it doesn't include the payments you make over the period or the compounding rate (when interest accrues on top of interest).

An interest calculator can help you include those elements in your calculations. You should also use the IRS tax forms, monthly statements, or amortization tables your lender can give you.

How interest expenses appear on your financial statements

Once you know how business interest expenses affect your financial statements, it’s easier to track the effect of interest on your business's finances – in particular, how these expenses affect your cash flow, net income, and profitability.

- Interest appears on your profit-and-loss statement as an expense.

- The interest you pay affects your balance sheet, but it doesn't appear on that report.

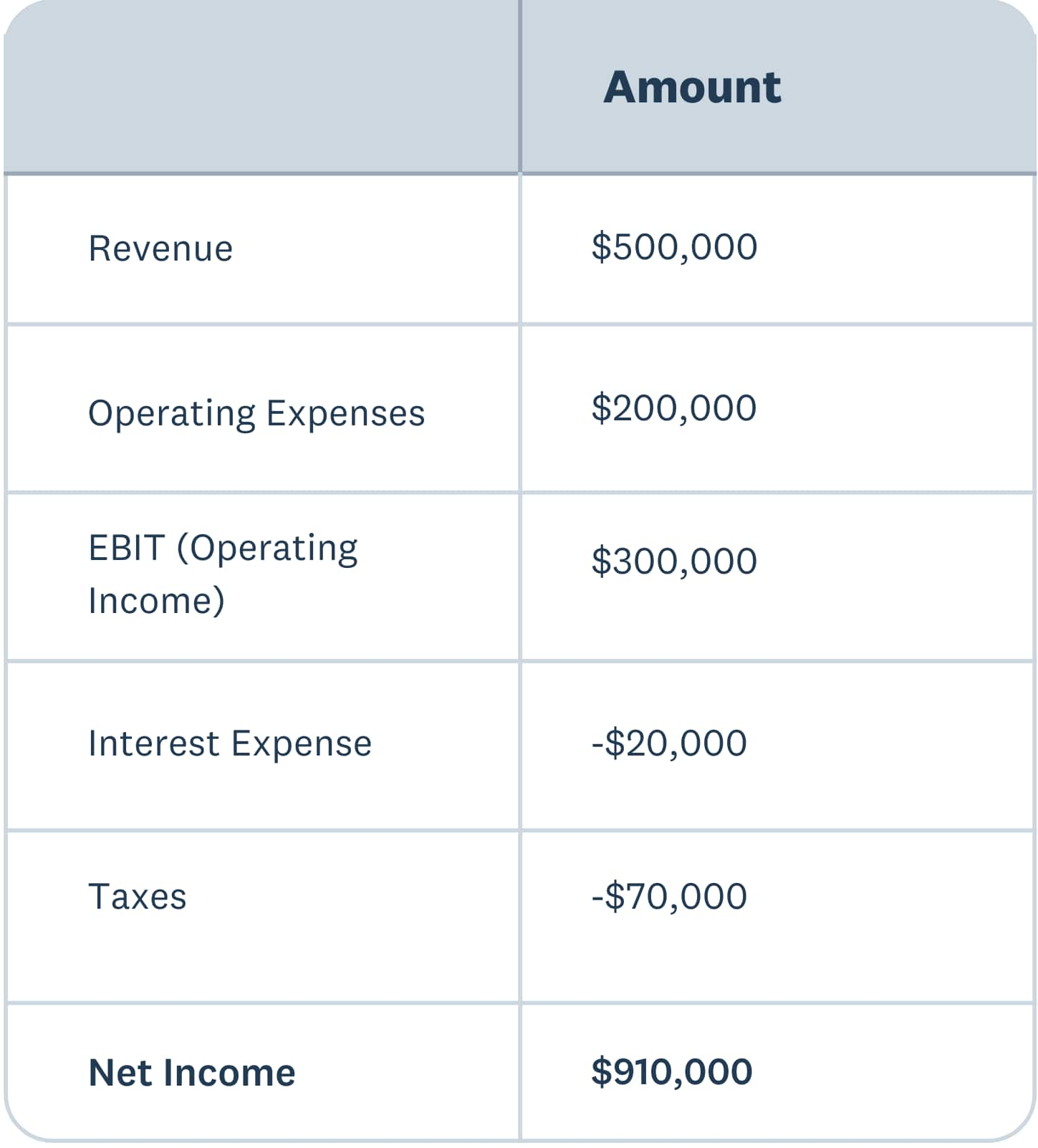

Interest expenses on your profit and loss statement (P&L)

Interest expenses appear as an expense in the non-operating expense section of your P&L.

This separation of the interest from the rest of your operating expenses:

- Lets you see how your debt loads and interest levels affect your profitability.

- Is useful if you're selling your business or bringing in investors – they get a stronger sense of your operational profits and can get a better idea of whether debt management could improve your bottom line.

Sample P&L with interest expenses:

Interest expenses on your balance sheet

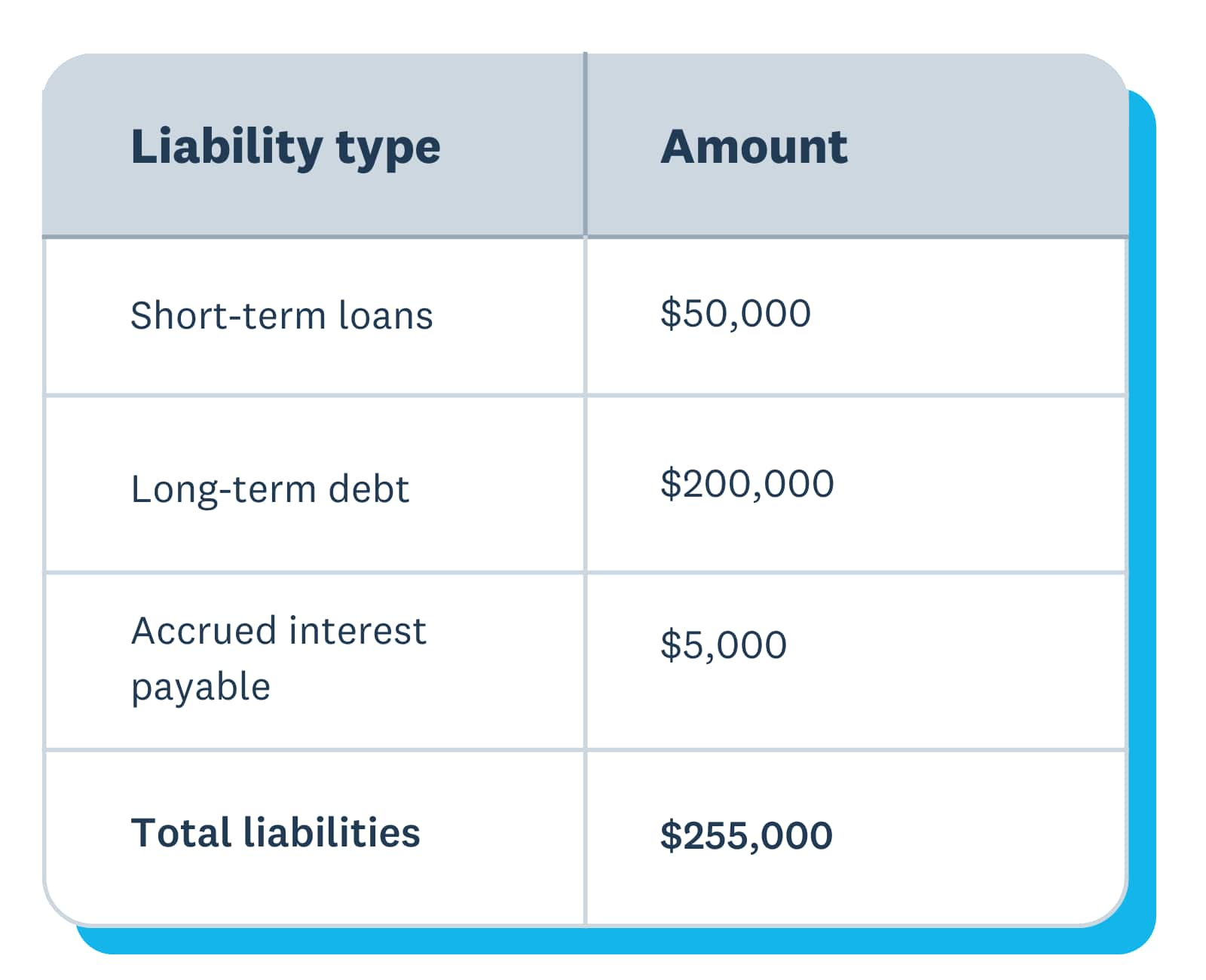

Your balance sheet doesn’t record interest you’ve paid – only the interest you’ve accrued and not yet paid. You enter it in the liabilities section of your balance sheet.

Say you take out a long-term loan for $200,000. You don't have to make payments for the first 6 months of the loan, and during that time, you accrue $5000 of interest. Your business also owes $50,000 in short-term loans.

When you look at your balance sheet 6 months after taking out the loan, it’ll show $200,000 as a long-term liability, $50,000 as a short-term liability, and $5000 in accrued interest.

All these numbers go together to calculate your business's total liability.

Table example: balance sheet liabilities section

Examples: how loan payments affect your financial statements

Here's a couple of examples of how loan payments might affect financial statements in practice.

1. Making a loan payment

When you make a loan payment, the entire payment affects your cash flow, but on your P&L statement you only report the interest portion of it.

Say you make a $2000 mortgage payment on your commercial property – $500 is interest and $1500 goes to the mortgage principal.

- The $500 interest goes on your P&L statement as an expense, along with all your other business expenses like wages, office supplies, and utility bills.

- The $1500 principal payment reduces the mortgage loan on your balance sheet.

2. When your loan payments cover only some of the interest due

What if your loan payments only cover a portion of the interest due?

Say you have a loan for $200,000, the monthly interest is $2000, but you’re only paying $1000 per month.

The entire $1000 payment gets posted to your P&L as interest. Since no portion of the payment is applied to the principal, the loan balance on the balance sheet remains unchanged. However, the $1000 accrued interest is recorded as an expense on the P&L once paid. Any interest unpaid remains on the balance sheet as interest payable in a liability account until paid.

Which interest expenses you can claim as tax deductions

Businesses can often reduce their tax bills by deducting interest on their business expenses from their taxable income. But larger businesses can face limits on the business interest they can claim back.

What you can claim: tax-deductible Interest expenses

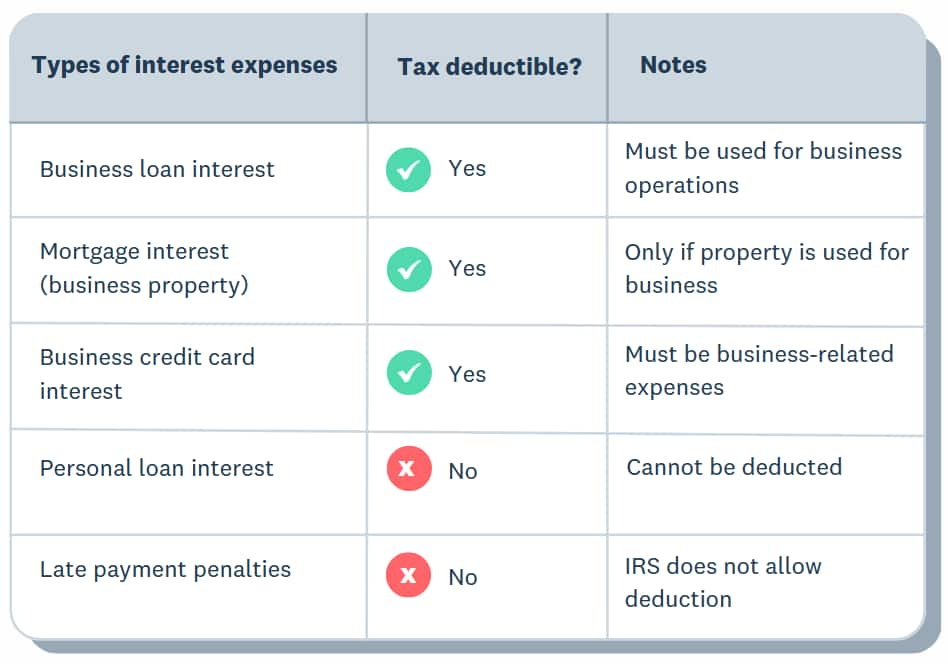

In general, the IRS allows businesses to deduct interest paid on:

- Business loans

- Mortgages on business property

- Business credit card debt

- Financing for business equipment

- Any other interest incurred for business purposes that isn’t exempt (see below).

The IRS doesn’t allow you to claim a deduction for late fees or interest incurred for personal reasons. You also can’t claim deductions for capitalized interest (which gets added to the value of your capital asset instead). It still reduces your taxable income, but over time instead of in the year you incurred the expense.

[Deductible vs non-deductible interest expenses]

Larger businesses might face limits on the interest they can claim

If your business had average gross receipts over $30 million in the previous 3 years, you might not be able to deduct interest over this threshold.

Regulations can change, so check with the IRS for the latest rules.

How to maximize your deductions

To make sure you get full credit for your interest expenses:

- Carefully track the interest you’ve paid

- Use monthly statements or annual tax forms to accurately record the interest you’ve paid

- Separate your business and personal expenses so you don't overlook any business interest

An accountant or financial advisor can give you the best advice on what your business can claim. You can find an advisor here.

Avoid common mistakes with interest expenses

Here are errors small businesses often make when recording, claiming, and dealing with interest expenses – and how to avoid making them.

1. Classify interest expenses incorrectly

Make sure the interest is deductible –you can't deduct interest on loans for overdue taxes, fines or penalties-related interest, or capitalized interest.

2. Documenting expenses poorly

Keep loan agreements and payment records so you can prove the interest expenses you’re claiming for tax purposes were incurred on business expenses.

3. Ignoring deduction limits

If your business is over the gross receipts threshold ($30 million for the previous 3 years), keep the deduction limits in mind.

4. Paying too much interest

If interest payments are stretching your business finances, think about refinancing loans to keep them under control.

5. Mixing personal and business interest expense

Keep your personal and business finances separate. To prevent you from accidentally claiming personal interest as a business expense, it helps to have separate business and personal accounts and credit cards.

FAQs on business interest expenses

How do interest expenses affect my cash flow?

Interest expenses are recurring costs that reduce your available cash flow. High interest payments can strain your liquidity, too, making it harder for businesses to cover operating expenses and invest in growth – so it makes sense to minimize your interest bill.

How do different loan structures affect interest expenses?

The business loan structures vary, but the most meaningful difference is between fixed-rate, variable-rate, and interest-only loans. With fixed-rate loans, interest rates are constant, so your interest expenses won’t change much between periods.

With variable-rate loans, your interest payments can change – sometimes quite dramatically – as the rates fluctuate with the market. If you have an interest-only loan, you’ll pay just the interest at first, so your payments will be lower until you start repaying the principal.

How does inflation affect my interest expenses?

Higher inflation often leads to higher interest rates, increasing borrowing costs – especially for businesses with variable-rate loans. If interest payments are biting into your cash flow, see if you can negotiate a better deal with your lender or move to an interest-only loan.

How can I manage high interest expenses for my business?

Businesses can reduce their interest expenses by refinancing to lower interest rates and by making extra payments to reduce the principal faster. You can also try to negotiate better terms with your lender.

It's always a good idea to talk with your financial advisor if you’re having trouble meeting your interest expenses.

What happens if my business defaults on interest payments?

If you miss interest payments you could be hit with late fees and penalties from lenders, at first. If you continue to miss payments, you might even face legal action or foreclosure if the loan is secured by assets. A history of missing interest payments can also affect your business’s creditworthiness, which can make it more expensive to borrow in future.

How should I report my business’s interest expenses for tax purposes?

Report the Interest expenses on Schedule C (sole proprietors), Form 1065 (partnerships), Form 1120S (S Corporations) or Form 1120 (C Corporations) as a deductible business expense. Make sure you’re following IRS rules and limitations when you do so. Download these forms from the IRS or use tax preparation software like Xero to help you file these forms.

What is the difference between prepaid interest and interest expense?

You pay interest expenses in arrears, while you prepay interest up front before the interest accrues. You record this prepaid interest on your balance sheet as an asset (a prepaid expense) – but it’s not tax deductible until you’ve paid it or it has accrued. Remember the interest expense definition: interest expenses are costs incurred for borrowing funds. So deduct interest as an expense in the period incurred, or pay it just like most other business costs.

Can I carry forward interest expenses to future tax years?

Yes – but only if your business is subject to the IRC limitations on larger businesses. If that’s you, then you can carry forward any disallowed interest expenses indefinitely – until you can deduct them in a future tax year. But if this doesn’t apply to your small business and the interest (along with other expenses) creates an overall loss for your business, you can roll forward the net operating loss.

What is accrued interest and how should I record it?

Accrued interest is interest that has been incurred but not yet paid by the end of an accounting period. It appears as a current liability on the balance sheet. If your business uses accrual accounting, record the interest as an expense on the income statement; otherwise, note it on the P&L until you’ve paid it.

Can I include interest expenses in the cost of inventory?

Yes. Under the capitalization rules, interest expenses on loans used to finance inventory production can be included in the cost of goods sold (COGS) for tax purposes.

Disclaimer

Xero does not provide accounting, tax, business or legal advice. This guide has been provided for information purposes only. You should consult your own professional advisors for advice directly relating to your business or before taking action in relation to any of the content provided.

Start using Xero for free

Access Xero features for 30 days, then decide which plan best suits your business.